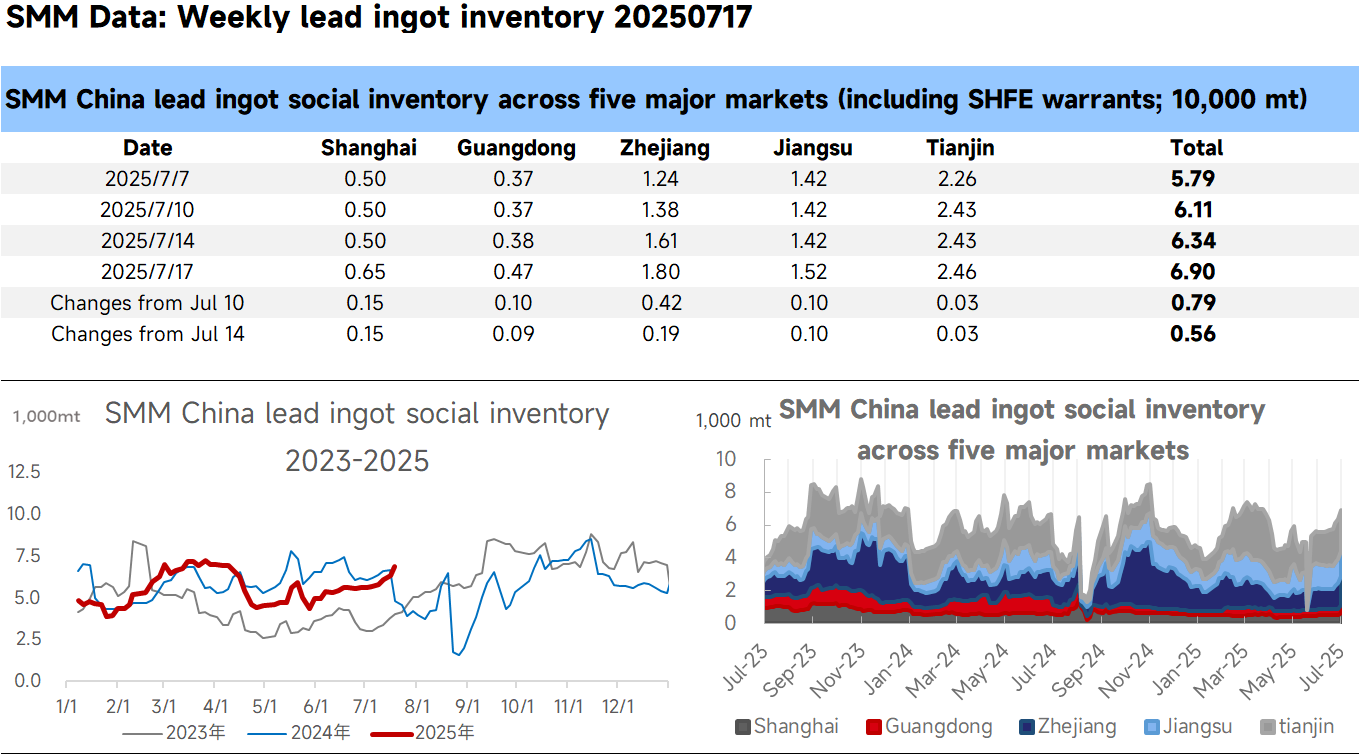

SMM News on July 17: According to SMM, as of July 17, the total social inventory of lead ingots across five regions reached 69,000 mt, an increase of 7,900 mt from July 10 and 5,600 mt from July 14.

This week, the SHFE lead 2507 contract completed delivery. The transfer of lead ingot inventory due to cargo pick-up led to a continued increase in social warehouse inventory of lead ingots, with varying degrees of increase in inventory across the five regions, primarily in warehouses in the Jiangsu, Zhejiang, Shanghai region. Recently, lead prices have been in the doldrums, with a decline in the enthusiasm for shipments from primary lead and secondary lead smelters. Additionally, maintenance and production cuts at some smelters have led to a tightening of regional lead ingot supply. For instance, the situation of smelters in Henan province queuing up to pick up goods has persisted from last week to this week. This week, the spread between futures and spot prices of lead narrowed day by day. The discount of electrolytic lead quotations from the main producing region of Henan province against the SHFE lead 2508 contract narrowed from a discount of 200 yuan/mt last week to a discount of 100 yuan/mt at the factory. Furthermore, the decline in lead prices has led to a further expansion of losses for secondary lead enterprises, dampening the enthusiasm for shipments and production at smelters. Enterprises have either suspended shipments or refused to budge on prices and offered shipments at a premium. Secondary refined lead quotations were offered at a premium of 0-100 yuan/mt against the SMM #1 lead price at the factory. With the conclusion of SHFE lead delivery and the narrowing of the spread between futures and spot prices, the movement of inventory by suppliers will be suspended. It is expected that the growth in social inventory of lead ingots will slow down. If the supply of lead ingots in Henan province does not recover next week, downstream rigid demand may shift to consuming social warehouse inventory.